What is your Money Funnel?

We've all heard about funnels in the online space, right? This is what online business people use to grab people's attention and then filter them down to sell them a product, service or whatever.

We all are familiar with the concept and mostly how to use them. Some of us more than others. Ha!

So, let's take that familiar concept and change the conversation to money. Cause in my little online world, its all about the Benjamins, baby. 💲💲

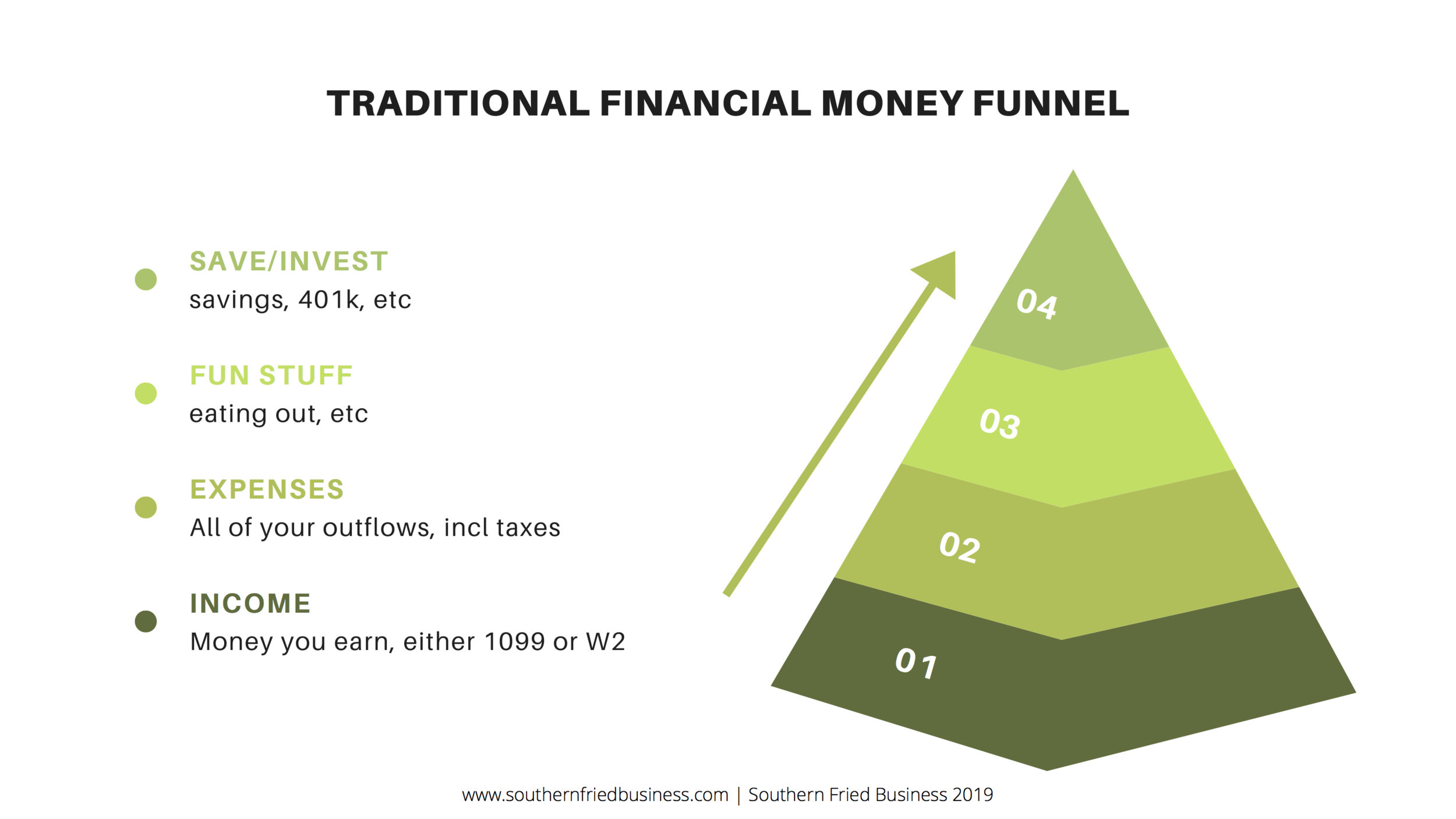

So, if we look at what traditional financial advisors tell you to do with your money... I've included a graphic below to help.

Normally, You start at the bottom of a funnel or pyramid, working your way up. And that holds true with money too. I’m a poet and didn’t even know it! No more rhymes - I mean it! Anybody want a peanut!?!? 🥜

Income. This is money you earn whether its through a job and W2, or through self employment/entrepreneurship, and a 1099, or maybe you have a combination of these two.

Expenses. These include all of your outflows, including your taxes.

Fun Stuff. Eating out, Target runs, travel, etc

Save/Invest. Once you've gone through the rest of the funnel, then you usually save what's left over.

Are you seeing the problem yet? You're a pretty smart chick, so I bet you are.

I'm about to turn your traditional money world upside down!

Want to listen in? Podcast link below 👇🏼🍎

So, what I've done is change the funnel to not only work from top to bottom, but I've also rearranged a bit. I'm calling it the Southern Fried Business money funnel. First, lets flip it. So, saving and investing is at the top. You're probably now asking me, “What the heck? How can I save if I don't know how much I'm making in income?” Hang on little grasshopper and I'll share the secrets of the universe with you.

My husband and I decided early on that we were going to save at least 30% of our annual income, working towards 40-50%. We also operate a year behind to get a year ahead. What the what? So, if we made $100K last year, we're committed to saving $30,000 this year. Now, we're a little flexible on this amount for a couple of reasons. First, we're both self-employed. So, that number could fluctuate - can anyone say COVID? Now, under normal circumstances, if we'd made $100K last year, we'd expect to make more this year. Even is our numbers trend lower, we will give up our fun stuff to hold true to our commitment. Second, what happens if our numbers go up? Then, that $30K will go up too. So, let's say we ended up making $250K, then our new savings number would end up at $75K, minimum. And now, we have a new basis for the next year. Our new savings minimum is now set at $75,000.

Sounds crazy right??? You're probably thinking, "now Connor, how will this work when I only make $30,000 per year. Or $50,000 per year? Or maybe $1,000,000 per year? Its the same equation sis. It works no matter where you are and how much you make.

And that ladies, is called PAYING YOURSELF FIRST. BOOM. MIC DROP! 💥🎤

Now we head into the income level. Just like the other funnel, its based on how much you earn in a year, whether your paycheck or your self-employed income. Not much else to say in this part of the funnel, except if you don't have more control of your earning potential, then you might need to examine your career. I understand there is a comfort in knowing how much you're bringing home each paycheck, but now you're trading your time for money. And if you have listened to my other podcast episodes, you'll know that time is the most expensive commodity around. Because no matter how much you make, you can't buy it back.

Next we're onto expenses. Full disclosure - I'm NOT a budgeting expert. Obviously, I'll tell you to spend less, where you can. Just like Marie Kondo tells us to get rid of our unwanted stuff, I'm telling you to Kondo and get rid of it - but just don't go and spend money to replace what you just purged. Duh! You know what to do.

And lastly, we have our fun stuff. This is true discretionary money because its the one piece of this puzzle that you can eliminate. We all like to do our thing. Eating out, shopping, travel, whatever floats your boat. But here's the thing, this part of your money funnel is not essential to your survival. If you want to guarantee you have fun money, then you need to work harder friend. Get a promotion, start a side hustle?

But me fussing at you about making what you're worth, I'll save that for another time.

Have I totally blown your mind? Have I inspired you to make some changes? Maybe you just think I'm a crazy gal with a weird accent. Whatever the case, I hope to see you next week for another episode that will FUND YOUR LIFE and OWN YOUR DESTINY.

In the meantime, remember what my Pappaw would say and don't take any wooden nickels!

Show sponsors:

👛 Save up to 75% off retail with preowned luxury accessories at Fashionphile. https://shrsl.com/2ft0j

📅 Want my best paper planner, but online? Head to https://artfulagenda.com and use my code RC54216.

💌 I love telling you stuff. But, I couldn’t figure out how to send consistent emails. Flodesk to the rescue! 💥 For 50% off of your Flodesk subscription, use my code https://flodesk.com/c/U89D30.